Working hard in the background...

8 Tips to Boost Your Credit Score in Canada

Published Apr 29, 2026 7:01 AM • 5 min read

Fact Checked

In many ways, our identity gets tied up in numbers. We’re assigned phone numbers, social insurance numbers, employee numbers, and – in the world of lending – credit scores.

These 3 digits (ranging from 300-900 in Canada) determine our trustworthiness to creditors based on factors like when we pay our balances, how much we spend, and how many credit products we pull from.

While we all want to be responsible with our credit all the time, the truth is, life happens. Unexpected payments pop up, employment can be inconsistent or scarce, and let’s face it, we’ve all been affected in some way by inflation.

So, what do you do when your credit score takes a hit?

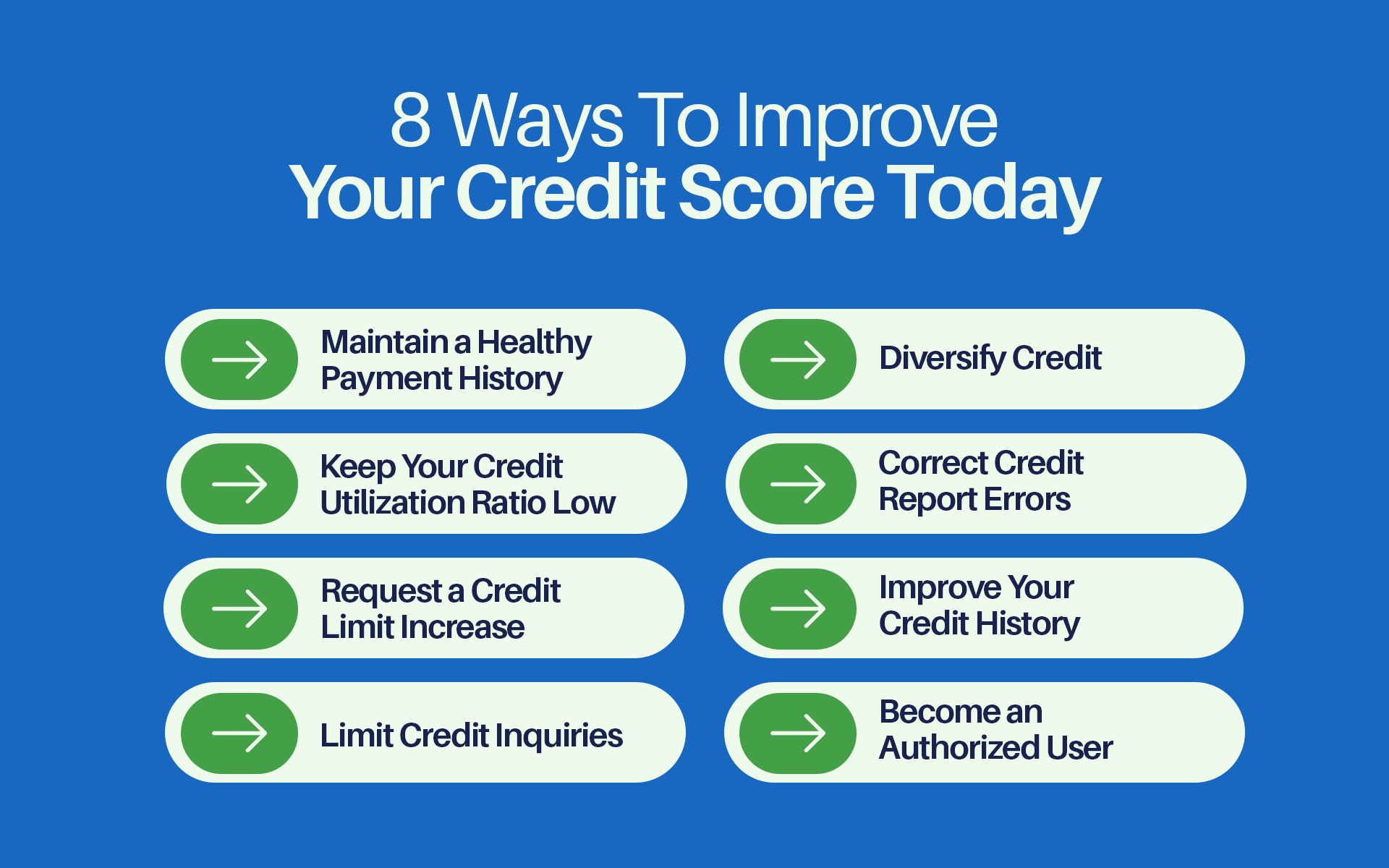

To help you get back on track, we’ve curated 8 ways to improve your credit score today, tackling strategies like responsible payment practices, credit management, and account initiatives.

Maintain a Healthy Payment History

The same way you should regularly check in with your physical and mental health, you should always set aside time to check in with your financial health as well.

A good way to review your payment history and any outstanding costs is to check your credit reports from Canadian credit bureaus – Equifax and TransUnion. We’ve covered Canadian credit bureaus in the past; find out more here.

Each bureau comes up with its own report, so check each respective provider. Inside your credit report, you’ll be able to scope out any inaccuracies or fraudulent activity and identify any unpaid balances in need of attention.

Once you’ve corrected or covered these current components (if applicable), you can start to follow these credit-conscious habits, encouraged by the Government of Canada:

- Make all your payments on time (in the case of credit cards, pay by your billing cycle’s respective due date – additional details available here)

- If you can’t cover the full amount owed, make the minimum payment on time

- If you suspect that you’ll have trouble paying an upcoming bill, contact your lender immediately to let them know and come up with a plan

- Never skip a payment, even when a bill is under dispute

Keep Your Credit Utilization Ratio Low

In addition to the tips listed in the previous section, when it comes to how much of your credit limit you spend, you should always keep your credit utilization ratio low.

Typically, financial experts recommend that spenders keep this ratio under 30%.

If you tend to use more than 30% each cycle, lenders might start to view you as a risky borrower, even if you constantly pay your balance in full and on time.

Request a Credit Limit Increase

If you’re having trouble keeping your spending under that 30% recommendation, consider requesting a credit limit increase. A credit limit increase will allow you to spend the same amount of money without dipping too deep into what you have available.

You’re more likely to have your request approved if you have a healthy payment history or your financial status has improved (for example, maybe you finally landed that well-deserved promotion).

Remember, though, even if your credit limit increases, you’ll want to keep your balance similar to what it was before so that it sits well below that 30%. Never view a credit limit increase as an excuse to overspend!

Limit Credit Inquiries

When you apply for a car loan, a mortgage, or even a brand new credit card, lenders tend to perform a hard credit check (or hard inquiry) into your credit report.

Hard credit inquiries can affect your credit score by slightly lowering them (by about 5 points or so).

One hard inquiry generally won’t make a huge impact on your credit score, but multiple at once certainly can.

The best way to limit hard credit inquiries is to first apply for new credit only when necessary and secondly, to either stagger your credit applications or apply for multiple loans or credit cards during the grace period. This “grace period” refers to a time frame where you can rate-shop for mortgages and loans and initiate multiple inquiries without majorly affecting your credit score. A grace period typically lasts up to two weeks and combines several hard inquiries as one.

To discover more about hard credit inquiries, as well as how they differ from soft credit inquiries, add this previous post to your reading list.

Diversify Credit

Sometimes, your credit score won’t budge because you only have one type of credit product.

Credit products include car loans, student loans, credit cards, and lines of credit.

Opening multiple credit accounts and balancing them well helps improve your creditworthiness and can increase your credit score as a result.

Correct Credit Report Errors

As briefly mentioned in the credit payment history section, you’ll want to review your credit report for any fraudulent charges or incorrect information.

If you come across any errors, you’ll need to dispute them with the associated credit bureau. Generally, disputes can be filed online, over the phone, by mail, or by fax.

Improve Your Credit History

Part of boosting your credit score means improving your credit history.

Your credit history refers to how long you’ve had and used a credit account. The longer an account is open and active, the more positive an impact it will have on your credit score.

While it may be tempting to close old accounts, consider keeping them around (especially those with no annual fees) and using them occasionally.

Become an Authorized User

Another potential strategy is becoming an authorized user on someone else’s credit card, ideally a responsible cardholder with a long, positive credit history. In Canada, however, not all issuers report authorized user activity to the credit bureaus — meaning the benefits are not guaranteed.

If you try this approach, confirm with the issuer first that authorized users are reported to both Equifax and TransUnion, and only do this with someone you fully trust. If the issuer doesn’t report, you won’t see any credit score improvement. For a more reliable path, consider opening your own secured or starter credit card.

Conclusion

Whether you’ve accidentally fallen behind on payments, had some unexpected expenses come up, or simply don’t have much credit history to begin with, there are many strategies available to enhance your credit score. These strategies range from making responsible repayments to savvy spending to regularly monitoring your accounts.

By following these 8 ways to improve your credit score, you can start advancing your financial footprint today.

Frequently Asked Questions

Credit utilization reflects how much of your total credit limit you’ve used compared to what’s available.

When you keep this utilization under 30%, you show lenders that you manage your credit responsibly and aren’t over-reliant on borrowed money. As a result, they won’t view you as a risky borrower.

If you’re worried about missing a payment, the first thing you should do is contact your lender to discuss your options.

If you can, ensure that you make all of your minimum payments on time to avoid compromising your credit health.

Always avoid skipping payments, even during disputes, as this can damage your credit score.

When you responsibly manage multiple credit accounts, you’re essentially telling lenders that you’re more than capable of keeping up with several loans and billing cycles.

Not only does this prove that you’re an excellent multitasker, but it also improves your credit mix, which is a factor in credit scoring.

That said, only open new credit accounts when necessary and when you’re financially stable enough to do so.

About the author

Sara Skodak

Lead Writer

Since graduating from the University of Western Ontario, Sara has built a diverse writing portfolio, covering topics in the travel, business, and wellness sectors. As a self-started freelance content ...

SEE FULL BIOAbout the editor

Lauren Brown

Editor

Lauren is a freelance copywriter with over a decade of experience in wealth management and financial planning. She has a Bachelor of Business Administration degree in finance and is a CFA charterholde...

SEE FULL BIO