Working hard in the background...

10 Tips For Managing Credit Card Debt Responsibly in Canada

Published Apr 30, 2026 8:21 AM • 10 min read

Fact Checked

As much as we wish it didn’t, debt happens, and it might keep happening if you don’t learn how to handle it properly.

In this article, we put together a crash course on how to manage credit card debt, complete with 10 tips for managing credit card debt responsibly in Canada.

Start reading to uncover valuable debt management strategies like budget building, popular repayment methods, credit counselling, and debt consolidation.

1. Build a Better Budget

To move forward, sometimes you need to go backwards – to the financial foundation of it all.

Chances are, straying away from your budget could be what got you into credit card debt in the first place. But don’t worry, budgeting is tricky, and losing track is common when you don’t make a plan that is both realistic and catered to you.

One thing that throws countless spenders off track is the belief that budgets need to be rigid. This rigidity is what creates tension, and tension is what turns budgeting from a guiding tool to dreaded deprivation.

As Jessica Morgan, personal finance writer, speaker, and founder of Canadianbudget.ca puts it in an insightful blog post: “A budget should never be static. It should be adjustable and change based on your experiences and as you improve your relationship with money.” Later, she adds: “Suppose you went over budget; it’s not a failure; view it as a learning opportunity. Don’t let any small hiccups along the way derail your process.” She concludes this thought by stating: “Making a budget is a trial-and-error process. It should be iterative and change from time to time.”

So, as Morgan suggests, going over budget and stumbling into debt is nothing more than a lesson. In a way, it’s also a wake-up call, indicating that your original budgeting method needs some tweaking.

Ultimately, the best way to climb out of this hole is to create a budget that complements your debt repayment plan.

A complementary budget consists of:

- Reviewing your financial situation and tracking your spending. Understand your current financial situation and record your spending habits to calculate which spending categories you prioritize the most, then shift priorities based on necessity.

- Find a budgeting method that works for you, whether that be digital budgeting backed by helpful apps or digital budget planners, paying with cash instead of card, or sticking to common strategies like the 50-30-20 rule (where 50% of spending goes towards the essentials like food and rent, 30% goes towards non-essentials like dining out and subscriptions, and 20% goes towards covering debt, and, someday, your savings). When dealing with debt, you might want to boost that 20% repayment category and put your non-essential spending on pause if possible.

- Keep tracking. This “trial-and-error process” needs to be monitored frequently to confirm its effectiveness. Don’t be afraid to re-adjust when necessary.

2. Try Out Some Popular Debt Repayment Strategies

There are two popular debt-relief strategies you can turn to: the avalanche method and the snowball method. Each of these strategies helps you target one form of debt at a time.

The avalanche method consists of paying off your balances with the highest interest rates first, then working your way down to those with the lowest interest rates. By covering the larger interest rates first, you can tackle the most expensive debt quicker.

Alternatively, the snowball method is when you repay smaller balances first and build your way up to the bigger ones. By starting with the least expensive forms of debt, the snowball method makes you feel productive and motivated to keep going. That said, this method could take a little longer and might cost more money in the long run, since your biggest debts with the biggest interest rates may be paid off last.

Read More: How to Get Out of Credit Card Debt

3. Automate Repayments

Manually making repayments allows for control, but automated repayments allow for consistency. Ultimately, the goal of automation is to avoid missed payments that lead to higher interest rates, late fees or other penalties.

There are a couple of ways automated repayments can work in your favour. First, if you prefer the manual route, you can still set up automatic reminders that tell you when to make your payments in a timely manner. Second, you can opt for automatic (or pre-authorized) payments that are routinely paid to your lender through online banking.

If you’re particularly forgetful, automatic payments will quickly become your best friend.

4. Stick to Cash

Using a credit card, debit card, or contactless payment method to make purchases has quickly become mainstream. Sometimes, however, the safest way to cover necessary expenses without dipping into your security fund is to revert back to cash.

When you shop with cash, you’re limited to the amount of bills or coins you’re carrying in your back pocket.

Witnessing the physical transaction of your money can also help you abide by your budget. Digital transactions, while convenient, can make spending feel more abstract. Sometimes, you need to actually feel your wallet get lighter to truly register your spending.

5. Consider a Second Source of Income

We get that one job can be tough to juggle as it is. However, if you’re able to, it might be smart to consider a second source of income to help you cover your outstanding debt.

Whether this additional source is a part-time job, a passive digital product, or any type of service or craft you’d like to sell on the side – every little bit counts.

6. Consolidate Your Debt

If tackling one debt at a time or managing multiple debts simultaneously seems too overwhelming, you can always turn to debt consolidation.

“In a debt consolidation program, you make only one payment per month, which your agency disperses to all of your creditors,” explains Jeff Schwartz, Executive Director of Consolidated Credit Canada in an online Q&A forum. “A single loan payment makes debt management simple.” Later, Schwartz specifies: “You can consolidate credit card debt, a personal loan, and other unsecured debts you may have.”

Different credit card debt consolidation strategies include:

- Debt management plans: Typically implemented by credit counsellors, these plans combine several debts into one reduced monthly payment to reduce or eliminate interest rates.

- Debt consolidation loans: These particular loans come with lower interest rates and assist you in paying off all of your higher interest credit card debts through a lump sum.

- Using one of Canada's best balance transfer credit cards: When in doubt, you can always transfer your credit card debt on a high-interest card to a low or no-interest balance transfer alternative. This consolidation method works best if you can pay off your debt within the chosen balance transfer credit card’s promotional period. See Balance Transfer Calculator here..

- Home equity consolidation: Homeowners can also repay their debt by tapping into their home equity. Home equity lines of credit sometimes offer lower interest rates than traditional credit cards. Note that this method essentially uses your home as collateral, making it a riskier route that could end in foreclosure.

7. Negotiate With Creditors

Debt looks a little bit different for everybody, so don’t be afraid to negotiate a customized repayment plan with your creditors.

In many cases, together, both you and your lenders can come up with a personalized plan that you can actually keep up with.

You can also ask for lower interest rates or pauses in the repayment process when experiencing financial hardship, such as job loss.

If you’re lucky enough to have an alternative repayment plan approved, make sure you honour your commitment. Otherwise, you may have a harder time receiving any grace in the future.

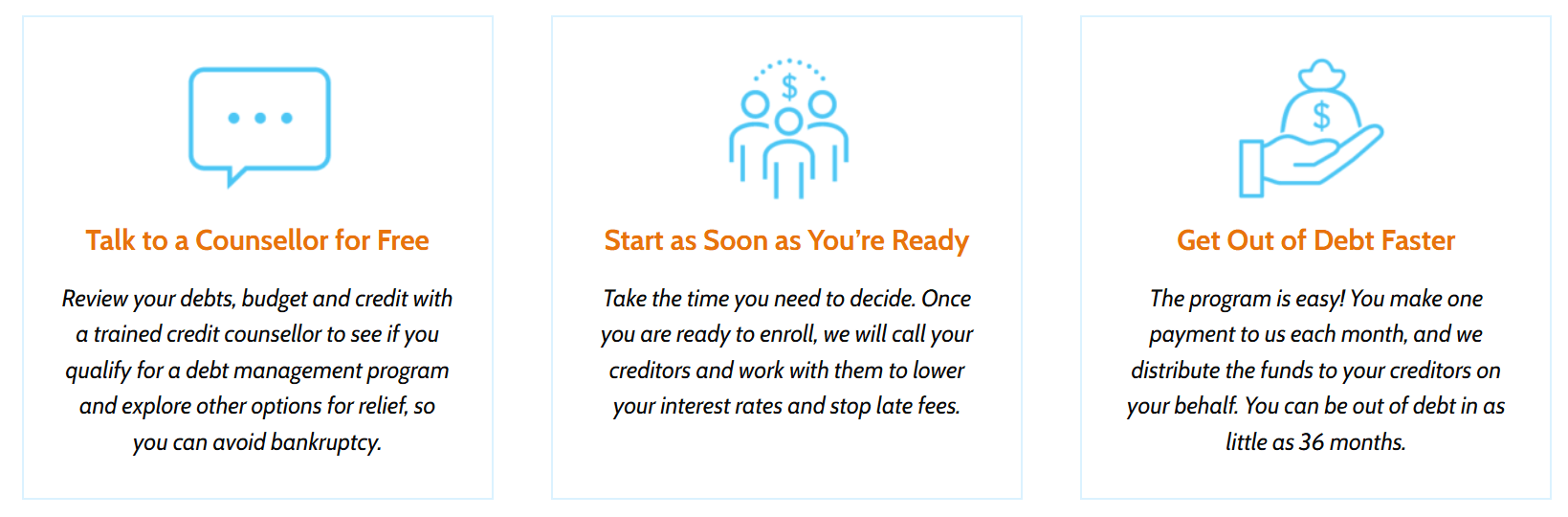

8. Turn to Credit Counselling

You never have to face credit card debt alone. Canadian credit counsellors are equipped to help you come up with a debt management plan that consolidates all of your debt into one place.

Non-profit organizations like Consolidated Credit Canada, review your debt, budget, and credit to help you create an attainable course of action. In fact, they’ll negotiate with your creditors on your behalf to score lower interest rates and avoid late fees.

Here’s a brief overview of their process:

Save 30-50% on interest payments

Reduce the high interest on your debt by consolidating it in one place.

Get a personalized debt management plan and a 50% discount on your setup fee.

9. File a Consumer Proposal with an LIT

If you have a surplus of debt that you just can’t seem to shake, you can also work with a Licensed Insolvency Trustee (LIT). These trustees will assist you in filing a consumer proposal, a legally binding process that has the potential to lower your debt substantially.

An approved consumer proposal can lead to debt consolidation, placing all of your included debts into one monthly payment. These payments are made to your LIT and are then passed on to your creditors. A successful consumer proposal may also lead to a repayment extension.

While a consumer proposal can negatively impact your credit score (at least for a few years), this type of hit is far less detrimental than bankruptcy.

Considering how daunting debt can be, when filing a consumer proposal, you’ll want to work with an LIT that is both professional and understanding – think of your relationship as a partnership. As Pamela Meger, Senior Vice President and Senior Manager at MNP Ltd puts it in a related post: “Selecting an LIT is not just about finding someone to handle your debt; it’s about building trust with a professional who will guide you through a potentially life-changing financial process.”

10. If All Else Fails, File for Bankruptcy

As a last resort, you can also file for bankruptcy. This type of action should only be taken if your debt is deemed insolvent by a Licensed Insolvency Trustee, meaning you simply cannot repay what you owe.

When surrendering to bankruptcy, understand that you may be required to liquidate your assets.

Additionally, bankruptcy tanks your credit score, becomes part of a permanent public record, and stays on your credit report for several years.

Conclusion

There are plenty of better ways to manage your debt beyond making minimum payments. When it comes to managing credit card debt responsibly in Canada, you can try conscious and adaptable budget-building, popular debt repayment strategies, debt consolidation programs, or seek guidance from Licensed Insolvency Trustees or credit counsellors.

In the end, don’t beat yourself up about debt. Instead, learn from the experience. Plus, you can always bookmark this blog post to avoid future financial setbacks.

Frequently Asked Questions

Choosing the best method to repay your credit card debt depends on your financial situation. Repayment strategies like the avalanche and snowball methods are a great place to start.

The avalanche method can potentially save you the most money overall since you’ll tackle the highest-interest debts first.

On the flip side, the snowball method helps you build up momentum by paying off your smallest debts first. The snowball method can be very motivating, but it might lead to more money spent overall on high-interest balances.

If you’re juggling multiple high-interest credit card debts, then debt consolidation can simplify the repayment process while also potentially lowering your overall interest rate.

For expert advice on the matter, consult a licensed credit counsellor.

Unfortunately, filing a consumer proposal affects your credit for up to 6 years from the date you file or 3 years after you complete your repayments – whichever comes first.

Keep in mind, however, consumer proposals have a short-term impact on your credit score and are generally less damaging than bankruptcy.

On this page

- 1. Build a Better Budget

- 2. Try Out Some Popular Debt Repayment Strategies

- 3. Automate Repayments

- 4. Stick to Cash

- 5. Consider a Second Source of Income

- 6. Consolidate Your Debt

- 7. Negotiate With Creditors

- 8. Turn to Credit Counselling

- 9. File a Consumer Proposal with an LIT

- 10. If All Else Fails, File for Bankruptcy

- Conclusion

About the author

Sara Skodak

Lead Writer

Since graduating from the University of Western Ontario, Sara has built a diverse writing portfolio, covering topics in the travel, business, and wellness sectors. As a self-started freelance content ...

SEE FULL BIOAbout the reviewer

Anthony Coles

Editor

Anthony started off a career in finance working for the largest staging company in the UK. Tasked with setting up a procurement department and costing up large projects building film studios required ...

SEE FULL BIO